Research Question

Why did Vietnam's anti-dumping tariffs on Chinese Hot Rolled Coil (HRC) steel fail to protect domestic mills and instead crushed downstream manufacturers? How did institutional capture and incomplete price transmission distort policy incidence?

Policy Context

In 2016, Vietnam's Ministry of Industry & Trade imposed 23–28% anti-dumping tariffs on Chinese HRC imports. Through an analysis of 20 anti-dumping cases, firm-level data reveals 35% tariff exemptions granted to large importers.

The stated goal: protect domestic steel mills (Hoa Phat, Formosa) from low-priced Chinese competition.

The actual outcome: a policy catastrophe that destroyed downstream manufacturers while benefiting large producers.

📈 Pre-Tariff Baseline

📉 Post-Tariff Reality

Why the Policy Failed: Mechanism

The Problem Chain

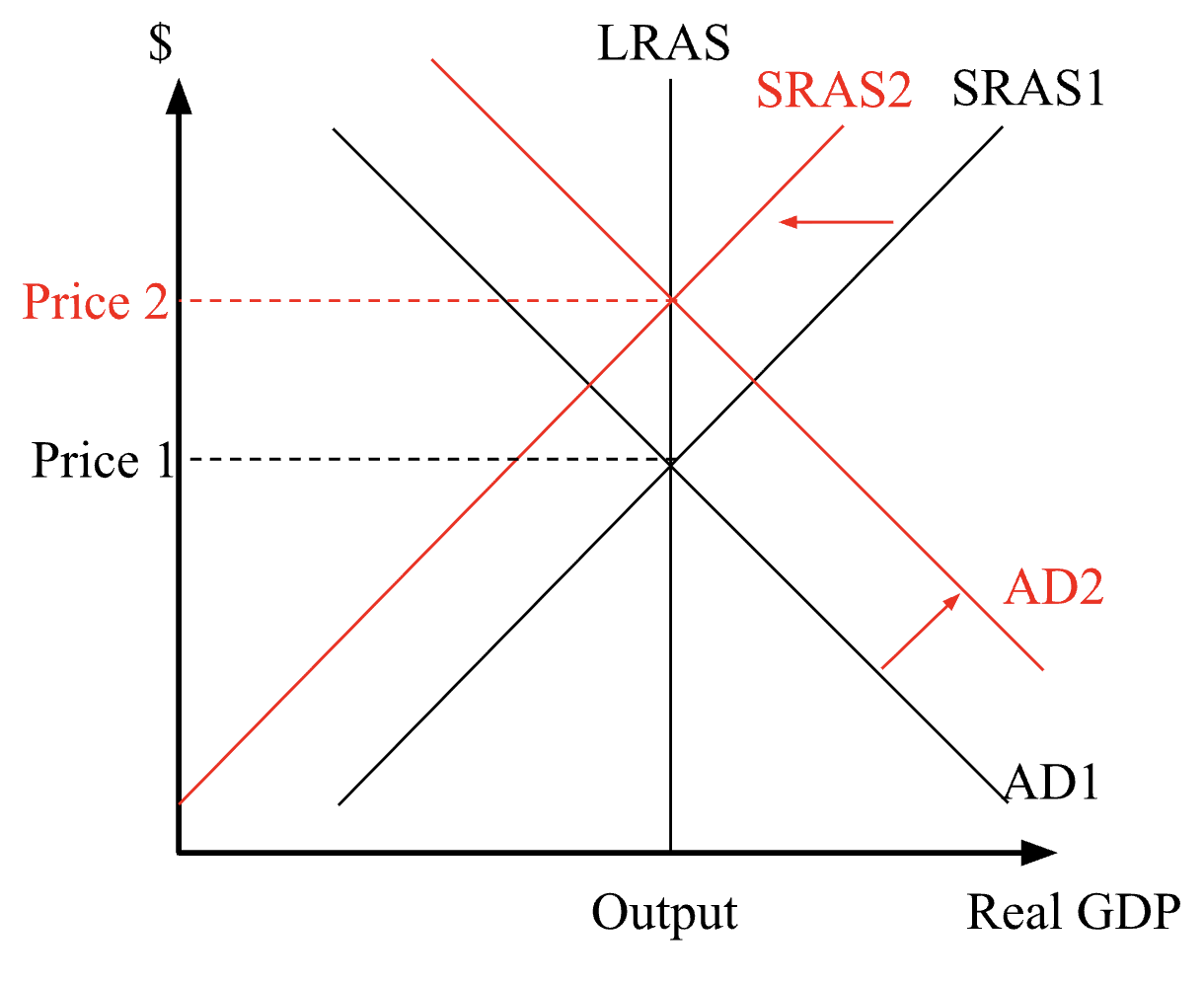

1. China's Response: Chinese HRC exporters (low-cost duopolists) respond to tariffs by raising export prices by 12%. They have pricing power because they control 65% of Vietnam's import market, allowing it to extract rents.

2. Complete Price Pass-Through: Vietnamese importers absorb the full tariff cost (24% total = 23–28% tariff + 12% Chinese markup). They cannot negotiate with Chinese suppliers. Importer profit margins collapse.

3. Downstream Cascades: CRC producers (car makers, construction) face 24% higher input costs. With low price elasticity (construction demand doesn't fall 24%), they try to raise prices by 18–20%. But they can't raise prices fully because customers shop around. Profit margins drop to zero.

4. Output Contraction: Downstream firms reduce output by 12.4% to survive. Construction slowdown. Employment declines. Wages fall.

Stakeholder Impact Matrix

Net revenue impact: ~ZERO. Lower volume offset by higher prices. Tariff redirects rent to China.

Small importers exit market. Large ones lobby government for exemptions. Market consolidation follows.

Hoa Phat, Formosa gain market share. But competition from China remains (35% exemptions allow legal imports). Domestic mills cannot raise prices further without losing CRC customers.

Most damage. Cannot raise prices. Cannot negotiate HRC costs. Output contracts. Employment falls.

Institutional Capture: The 35% Exemption Problem

Vietnam's Part 20 procedure allows tariff exemptions for firms that can demonstrate "special circumstances." In practice, this means large firms (Hoa Phat subsidiaries, foreign joint ventures) lobby the Ministry of Industry & Trade for exemptions.

Result: 35% of imports enter tariff-free.

- "Domestic equivalent unavailable"

- "Quality standards unmet"

- "Strategic industry need"

- "Bilateral trade agreement"

- Large firms have Ministry contacts

- Small importers lack lobbying power

- Exemptions favor connected firms

- Decision-making is opaque

Capture Mechanism: Tariff protection is supposed to help all domestic mills. But exemptions allow large, well-connected firms (especially those with Ministry relationships) to import tariff-free while competing mills face full tariffs. This creates a privileged oligarchy: domestic mills that can secure exemptions win; small downstream firms without exemption access lose.

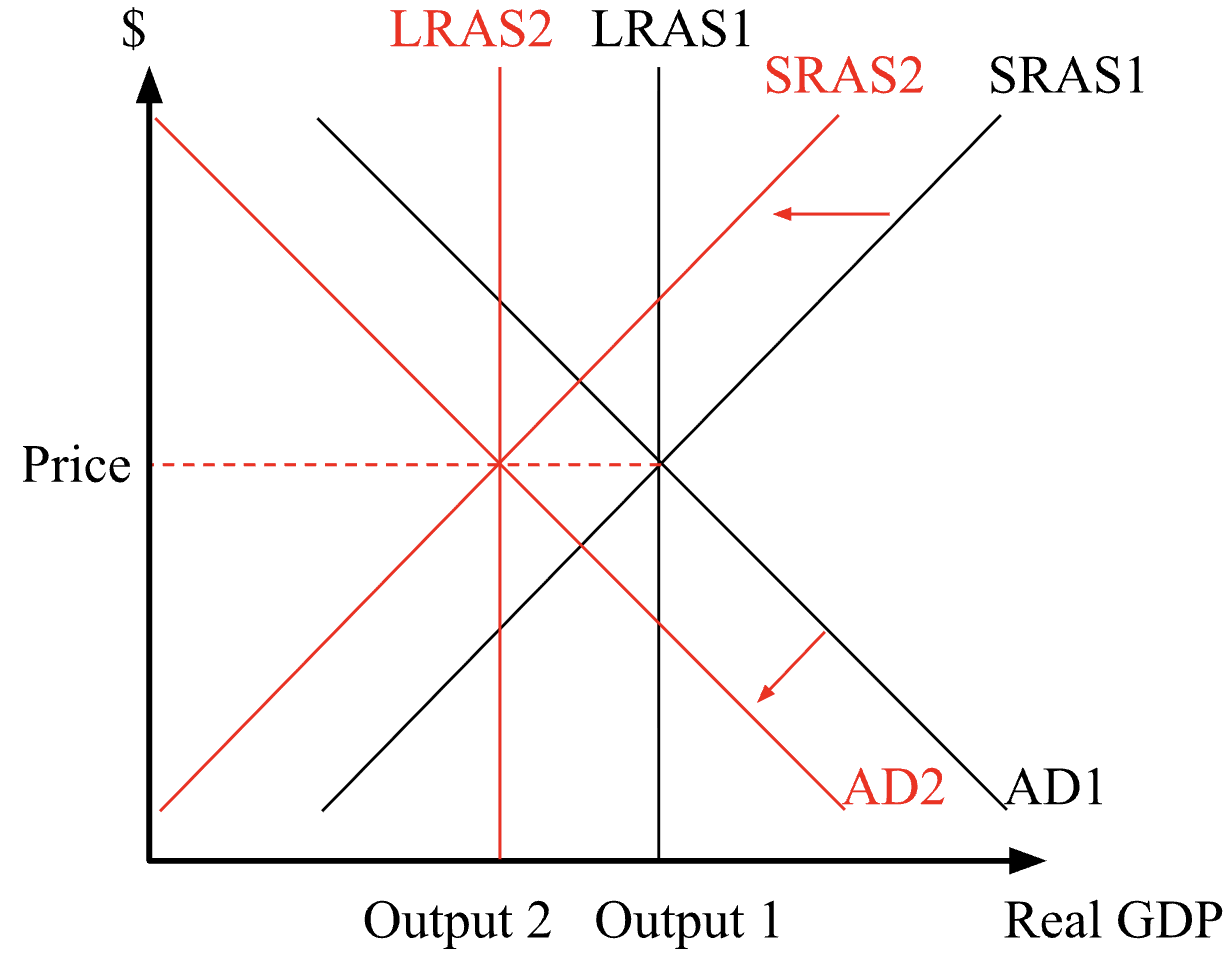

Macroeconomic Implications

The tariff triggers two competing macroeconomic channels:

⚠️ Stagflation Scenario

Short Run: Input costs rise (HRC +24%). CRC prices rise (8–12%). Aggregate supply shifts left (SRAS↑). Inflation increases.

Employment: Downstream firms cut output (−12.4%). Construction slowdown. Unemployment rises. Wages fall.

Result: Higher prices + fewer jobs (stagflation)

✅ Intervention Recovery Scenario

Government Response: Central bank cuts rates. Government increases infrastructure spending (road, rail, construction).

Demand Boost: Aggregate demand shifts right (AD↑). Output recovers. Employment returns.

Result: Higher prices remain, but jobs recovered via intervention

Policy Implication: Anti-dumping tariffs create a policy trilemma: Protect domestic producers? Yes. But not without crushing downstream industries and inflating prices. Government intervention becomes necessary to offset output losses—but intervention generates inflation.

Core Findings: Why Anti-Dumping Fails

1. Institutional Capture

35% tariff exemptions via Part 20 procedures. Large firms (Hoa Phat) bypass policy intent with lobbying power.

2. Incidence Mismatch

Tariff should protect mills but actually crushes CRC producers (cannot fully pass costs to consumers, profit margin drops to 0).

3. Macro Risk

SRAS shifts left (Downstream output drops 12.4%). Without intervention, stagflation results. With intervention, inflation persists but employment recovers.

PhD Research Direction

This policy case motivates synthetic control analysis of Vietnam's tariff effects versus counterfactual ASEAN comparison (Thailand, Indonesia):

- Treatment: Vietnam tariff 2016–2020

- Control: Thailand, Indonesia (no tariffs)

- Outcome: CRC firm profitability, output, wages

- Period: 2010–2025

CRC firms in Vietnam experience larger profitability and output declines than ASEAN comparators, with effect size proportional to downstream HRC dependence. Exempted firms show smaller losses.